What if we could align the way public company boards govern capital allocation with the way their CIO manages technology investments?

Public company boards don't approve every capital expenditure. They set allocation frameworks, define risk appetites, and measure returns. They govern portfolios, not projects.

Yet most CIOs still present technology as budget line items, a list of systems, initiatives, and headcount, rather than as a managed portfolio of investments with different risk profiles and expected returns.

This misalignment creates a disconnect between how boards think about capital and how technology leaders prioritize and present their work. It's one reason technology struggles to get the strategic attention it deserves in the boardroom.

The intellectual foundation

In Impact Intelligence (October 2024), Sriram Narayan makes a compelling case that technology investments should be managed the way investors manage financial portfolios, with deliberate allocation strategies, clear return expectations, and continuous rebalancing based on performance.

This isn't new thinking in finance. Harry Markowitz won the Nobel Prize in 1952 for Modern Portfolio Theory, which showed that diversification across assets with different risk-return profiles produces better outcomes than concentration in any single investment.

The same logic applies to technology. A portfolio approach balances high-growth bets, efficiency plays, risk mitigation, and strategic options, each serving a different purpose, each measured differently, each contributing to overall enterprise value.

Yet in most organizations, technology investments aren't managed as a portfolio. They're managed as an undifferentiated backlog, competing for the same pool of capital without regard to strategic purpose or expected return.

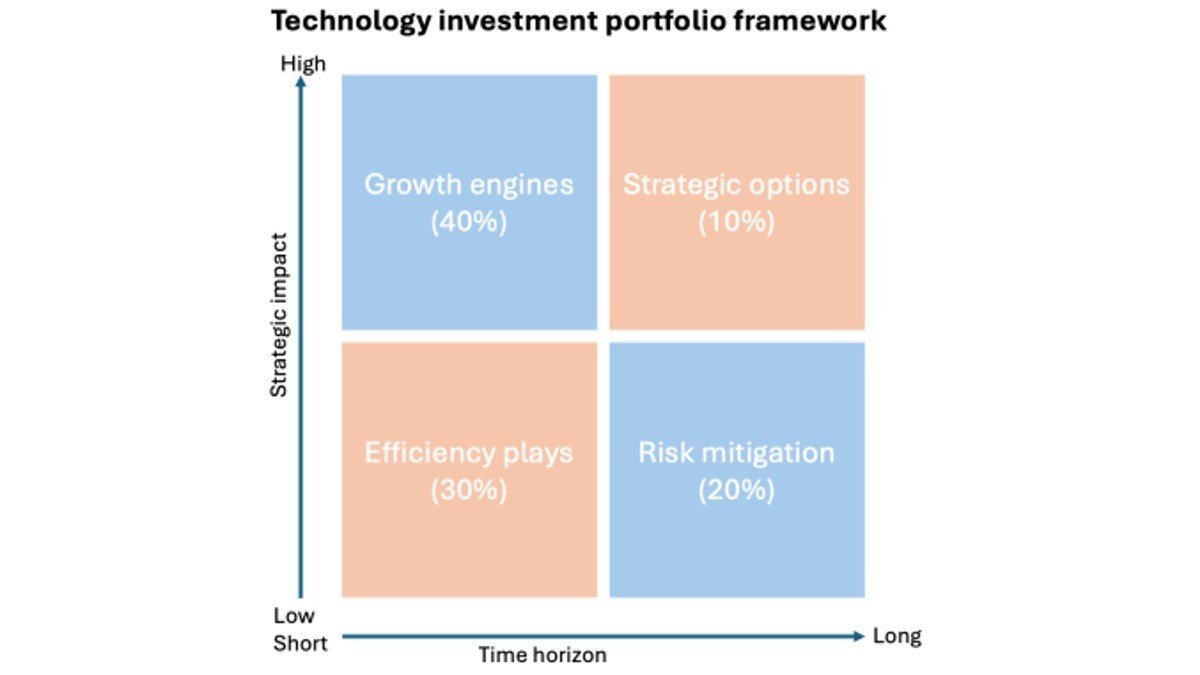

The framework: technology investment portfolio

I've deployed this framework across Fortune 500, very large enterprises and PE-backed healthcare and services companies to shift the conversation from "what projects are we doing" to "how are we allocating capital to drive enterprise value."

Four investment categories, each with different risk profiles, time horizons, and measurement criteria.

Growth Engines (40% allocation)

Technology investments that directly enable revenue growth, market expansion, or competitive differentiation. These are top-line drivers that show up in earnings calls.

Examples: Customer-facing platforms, data products sold to clients, AI-enabled services that create new revenue streams, digital channels that expand market reach.

Measurement: Revenue enabled, customer acquisition cost, time-to-market, competitive position.

Efficiency Plays (30% allocation)

Technology that reduces cost, increases productivity, or improves margins. These are EBITDA drivers that create operating leverage.

Examples: Process automation, workflow optimization, supply chain improvements, AI-enabled workforce productivity tools.

Measurement: Cost reduction realized, productivity gains, margin improvement, payback period.

Risk Mitigation (20% allocation)

Technology that protects enterprise value by reducing regulatory, cybersecurity, operational, or compliance risk. These investments prevent value destruction.

Examples: Cybersecurity infrastructure, regulatory compliance systems, business continuity capabilities, data governance platforms.

Measurement: Risk exposure reduced, incidents prevented, audit findings, regulatory compliance metrics.

Strategic Options (10% allocation)

Exploratory investments that create future optionality, technologies or capabilities that may become growth engines or efficiency plays as markets evolve.

Examples: Emerging AI capabilities, new technology platforms, proof-of-concept initiatives, market experiments.

Measurement: Learning velocity, pivot speed, capability development, strategic insights gained.

The critical fifth element: measurement and feedback loops

The framework only works if you build in constant measurement and feedback loops. Like any investment portfolio, you need to track actual returns, compare them to expected returns, and rebalance accordingly.

This means quarterly portfolio reviews with the executive team, evaluating what's delivering and what's not. Clear kill criteria for underperforming investments; if the returns aren't materializing, stop the investment and reallocate capital. Dynamic rebalancing based on market conditions, competitive pressure, and strategic priorities. Leading and lagging indicators for each investment category, so you see problems before they show up in financial results.

Without this discipline, the portfolio becomes static, a planning exercise that doesn't reflect reality. With it, you create a living capital allocation model that responds to evidence and drives accountability. In the past we could have an annual planning cycle. The world moves too fast today to not adjust quarterly, or quicker.

What this looks like in practice

At a large health system and at a multi-state medical group, we managed technology as an enterprise value portfolio across the whole company.

Growth engines included patient access platforms and telehealth capabilities that expanded market reach and drove incremental demand, enabling revenue growth in new service lines.

Efficiency plays included revenue cycle optimization and supply chain automation and consolidation that delivered measurable margin improvement, work that showed up in quarterly earnings discussions.

Risk mitigation covered cybersecurity infrastructure and regulatory compliance systems that protected the organization from material risk events in a highly regulated industry.

Strategic options included clinical decision support and emerging care delivery models that created future optionality as healthcare payment models evolved.

Every quarter, we reviewed the portfolio with the CFO and the entire executive team. Investments were rebalanced based on performance, market conditions, and strategic priorities. Underperforming initiatives were stopped, and capital was reallocated to higher-return opportunities.

The framework changed the conversation. Instead of defending technology budgets, we were discussing capital allocation strategy.

Instead of presenting project lists, we were showing how technology investments contributed to enterprise value across growth, margin, and risk.

The board-level question

If you're a CIO, here's the question to bring to your next board meeting or executive leadership discussion:

"How should we allocate our technology capital across growth, efficiency, risk mitigation, and strategic options to maximize enterprise value?"

That's the conversation that positions technology as strategic capital allocation, not as an operational cost center.

And if you're a board member or CEO, here's the question to ask your CIO:

"Show me our technology portfolio. What percentage is allocated to growth versus efficiency versus risk? What returns are we seeing? What are we stopping because it's not delivering?"

That's the governance conversation that aligns technology investment with fiduciary responsibility.